Register here to join our upcoming webinar on the new CIA Mortality Improvements scale (CanMI-2024).

Navigating the short and long-term impacts of COVID-19 remains a head scratcher in the actuarial world, where the only unanimous agreement is the absence of any definitive consensus. The Report to the CIA’s Project Oversight Group on Mortality Improvements Research (the “report”) asserts that “excess mortality directly and indirectly due to COVID-19 is a multi-year phenomenon” and that “COVID-19 related excess mortality introduces greater uncertainty in predicting future mortality”. Nevertheless, the model set forth in the report is calibrated to pre-pandemic data, and gives no flexibility to the user to reflect any changes to their future outlook on mortality improvements as a result of the COVID-19 pandemic.

The report states that calibrating a projection model to “experience data that includes periods with COVID-19 related excess deaths … is taken to be egregiously wrong”. This is a bold statement. We do not believe it is universally true1, but we agree with the sentiment if the data in mind has seen significant recent changes to mortality rates that are not expected to continue in the long run. However, we also think it is unlikely that the pandemic has had no effect on future mortality rates. If actuaries decide to base their future mortality projections on pre-pandemic calibrated improvements, it should be an active and documented decision.

In this instalment of our multi-part series covering the recently released CIA report, we explore the pandemic’s profound impact on mortality and whether mortality assumptions need to be adjusted for COVID-19. Although most health agencies have declared the pandemic over, there is little doubt that the lingering effects of the pandemic continue to drive today’s excess mortality in emerging Canadian population data. In this article, we will dive into the following key considerations:

- We will discuss three approaches being used to reflect possible impacts of the COVID-19 pandemic on future mortality rate projections, how these approaches can be modeled using baseline and/or improvement assumptions and discuss the limitations of using the new CIA model without the ability to make adjustments for changing future outlooks on mortality improvements.

- We will explore Canadian population-level excess mortality between 2020 and early 2022. At the beginning of the pandemic excess deaths were mainly driven by COVID-19 recorded deaths, but more recent data suggests a significant increase in non-COVID related deaths. Could other, less transient, factors such as ongoing strains on healthcare systems, delayed treatments, and potential long-term health complications among COVID-19 survivors be driving recent excess? And does this affect our future outlook for mortality improvements?

- In our previous instalment Socio-economic differences in mortality improvements, we explored differences between general population level data and data covering insured lives and defined benefit (DB) pensioners. Here we will explore the difference in COVID-19 mortality between different groups. Early pandemic data suggests that there was an insulation effect of the DB population, does that lessen any expected impact of COVID-19 on future mortality rates for this group?

The new CIA model is calibrated to data between 1980 and 2019. We have already discussed in detail in our article on Drivers of mortality improvements, the considerations needed when projecting historical data into the future. This question becomes even more relevant when trying to project mortality rates out past an unprecedented mortality event such as the COVID-19 pandemic. The CIA has highlighted its desire to complete further research on this subject, which we welcome. Given the amount of uncertainty introduced by the pandemic, we suggest that it is appropriate to introduce some flexibility over calibration parameters into the model to allow practitioners the ability to reflect a range of reasonable outlooks for future improvements. This would align with the approach taken by the Continuous Mortality Investigation (CMI) in the UK, on whose work a lot of the research in the CIA’s report is based.

A framework for the future impact of the pandemic

Determining life expectancy involves considering two key components: the baseline assumption and the improvements assumption. The baseline assumption relies on historical data, offering a snapshot of current mortality, without assuming any future change to mortality. The improvements assumption reflects anticipated changes in mortality rates over time; it tends to be a more subjective measure and should incorporate the impact of key drivers influencing changes in mortality over time, such as advancements in healthcare, changes in lifestyle or technological discoveries.

When determining mortality assumptions, it is important to ask yourself whether you think the underlying data is representative of what you are trying to model. With regards to the baseline assumption, is the data representative of the current mortality for individuals currently alive in your population? With regards to improvements, are the changes observed in your data representative of how things will change in the future (either in the short or long term)? If the answer is no, then data driven models will need to be treated with extreme care, and out-of-model adjustments may be appropriate.

There has been an emergence of three approaches to modeling post pandemic mortality:

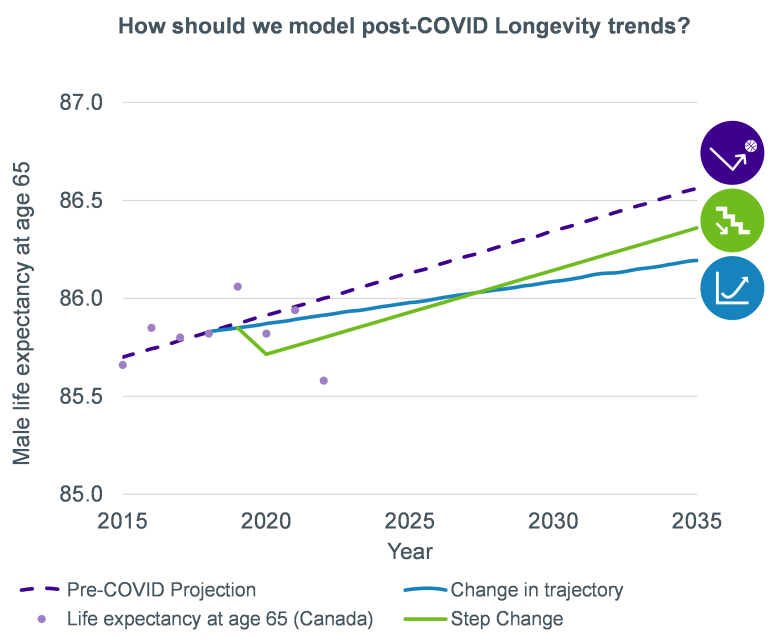

- The bounce back approach: This approach assumes that, after a few years of heavy mortality, mortality rates bounce back to the rates projected before the pandemic. It assumes the pandemic had an entirely transitory effect on mortality rates with no lost years of improvements. Any ongoing COVID deaths would be assumed to displace other causes of death and there would be no other long-term impact of the pandemic. To use this approach, you could use baseline and improvement models calibrated to pre-pandemic data, possibly with some out-of-model adjustments to allow for extra deaths in the transition period.

- The step change approach: This approach involves a short-term adjustment to base rates, followed by improvements continuing with the same trajectory as before the pandemic. It recognizes COVID as a new major cause of death (without entirely being mitigated by displacement of other causes of death), but that COVID will not impact the rate of future improvements (i.e., in comparison to pre-pandemic expectations, COVID has no impact on future medical breakthroughs, lifestyle changes, etc.). To use this approach, you could use a baseline assumption with an allowance for the new level of post-shock mortality, paired with improvement models calibrated to pre-pandemic data.

- The change in trajectory approach: This approach assumes that the trajectory of improvements in life expectancy will change from pre-pandemic expectations as a result of the pandemic. It acknowledges the pandemic’s impact on the pace of mortality improvements, supposing that COVID has lingering affects on various areas such as long-term health, medical advances or availability of medical services. To use this approach, you would need to adjust improvement rates away from pre-pandemic calibrated models.

We illustrate how male life expectancy at 65 will progress under each of these approaches in the chart below.

Under this framework, the new CIA model would produce improvement rates compatible with the bounce back approach (if used together with a pre-pandemic calibration of a base table) or the step-change approach (if used together with a base table reflecting the expected step change in mortality), indirectly asserting that improvements seen before the pandemic will likely persist into the post-pandemic era. Comparing to other widely used models: the latest Society of Actuaries MP model (US) aligns with the bounce back and step change approaches; the latest CMI improvements model (UK) can be used with all these approaches by adjusting the input parameters, although the core calibration aligns with the change in trajectory approach.

As many stakeholders seek to incorporate the effects of COVID on future mortality, the selection of the modeling approach will rely on the assessment of the post-pandemic outlook, potentially resulting in a blend of different approaches.

Potential impacts of the pandemic

There are a number of potential long-term effects from the pandemic that could lead to changes in life expectancy. Some of these may contribute to longer lives (such as the acceleration of medical advances from the development of mRNA technology) and some may contribute to shorter lives (such as impaired long-term health for survivors of COVID-19). We explored the future trajectories for various different pandemic scenarios in our paper: COVID-19 longevity scenarios: a bump in the road or a catalyst for change? Some of the key considerations in understanding how this might develop in the future are set out below.

The recent Canadian excess mortality conundrum

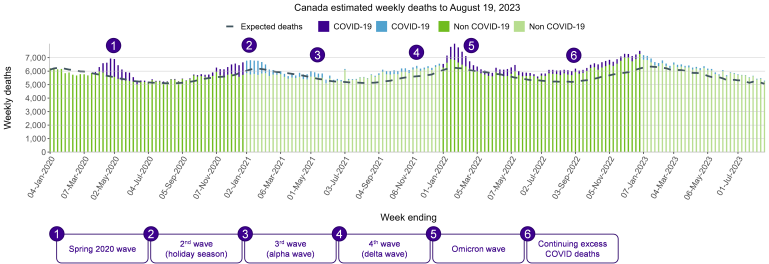

Canadian excess deaths (based on pre-pandemic expectations) have been persistently elevated since the beginning of the pandemic, with the first wave hitting Canadians in March 2020. The chart below shows the estimated weekly deaths between January 2020 and August 2023 for the Canadian general population (we note that the timing and magnitude of the pandemic waves will also vary by geographic region of Canada). The dotted line depicts the deaths in those weeks that were expected before the pandemic, calculated and published by Statistics Canada based on 2016-2019 data. Excess deaths are all deaths above the expected deaths dotted line in the chart.

The chart illustrates two key observations:

- Up until the beginning of 2022, COVID-19 was the primary cause of excess deaths,

- Following May 2022, excess deaths were predominantly attributed to other causes of death.

Source: Statistics Canada (Table 13-10-0792-01). Data is limited for the following provinces: MB data until December 3, 2022, NB data until July 22, 2023, NS data until May 6, 2023 and ON until July 15, 2023.

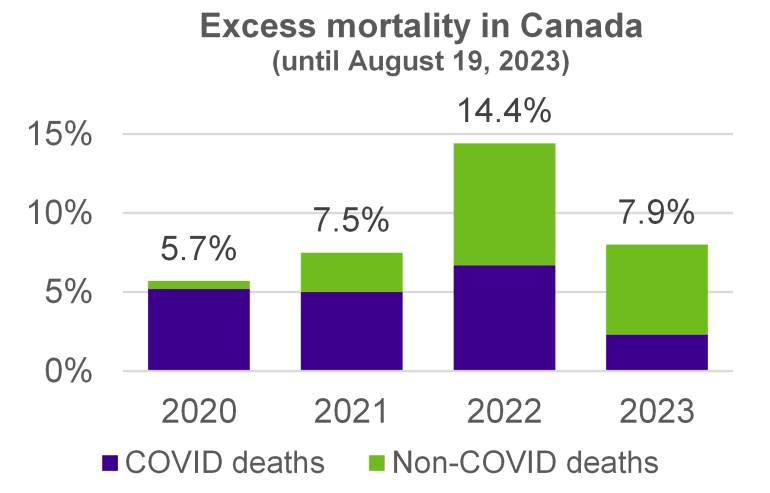

Summarizing this data, the following chart depicts Canadian excess mortality split between COVID (purple) and non-COVID (green) related deaths.

We observe an uptick in excess mortality levels between 2020 and 2022, followed by a decrease in the first part of 2023, but excess mortality continues to linger at elevated levels. This is dissimilar to the trends observed in both the US and the UK, where significantly higher mortality levels were observed in 2020 and in 2021, followed by an earlier decrease in excess mortality beginning in 2022.

So, what is causing these persistently elevated excess deaths levels? Our Canadian webinar2 on excess mortality navigates this question and explores whether these patterns are expected to continue. While recognizing that there are other possible explanations for non-COVID related excess deaths, our panel of industry experts highlighted the following major drivers of current and future mortality levels:

- Immediate impact of COVID-19 (i.e. COVID as a new cause of death, new strains of COVID);

- Long-term effects of COVID-19 such as COVID-19 complications, comorbidities, long COVID;

- Delays in treatment and preventative care resulting in growing waiting lists and a surge of deaths while waiting; and

- Strain on healthcare systems (i.e. increased workload and poorer mental health of healthcare workers, health workforce shortages, challenges in delivering care).

The CIA’s report has acknowledged that excess mortality directly and indirectly due to the pandemic is a multi-year trend, and assuming mortality will continue at pre-pandemic levels is an assumption that cannot be underwritten with conviction.

Impact on survivors

A so-far unanswered question about the pandemic is what the effect will be on the survivors. On the one hand, some assert we will see a survivorship effect, where the healthiest people will survive the pandemic resulting in a longer living population. On the other hand, others assert that we will see a scarring effect, where longer term health impacts resulting from many people contracting and recovering from the SARS-CoV-2 virus will result in shorter lives overall. There is not enough post-pandemic data yet to comment on how the balance of these effects will develop, but it is the populations that were most affected by the pandemic that will be most affected by the resulting effects.

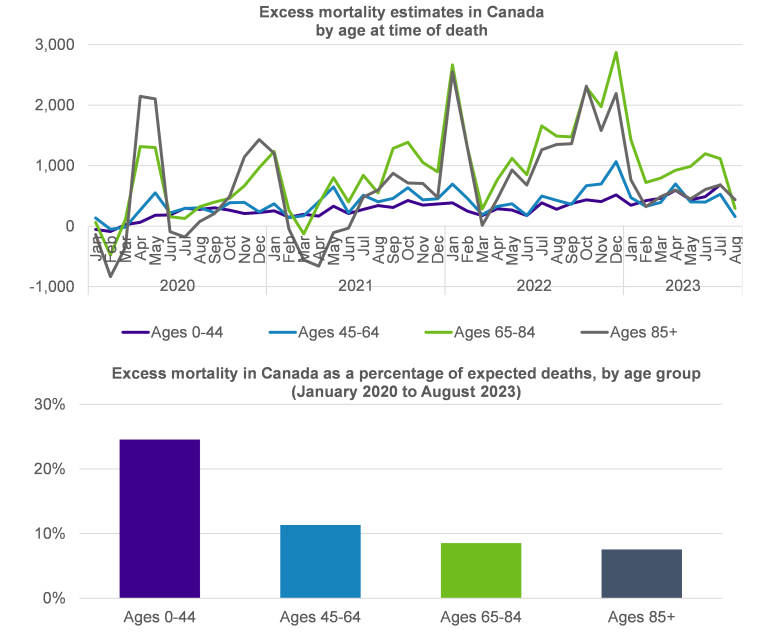

The charts below illustrate Canadian excess mortality by age group.

The top chart shows that the number of excess deaths was concentrated at older ages (grey and green lines), while the bottom chart illustrates that the most significant increase in excess deaths was at the youngest age group (purple bar). This is not surprising since expected deaths at younger ages are typically low, meaning that even a small change can have a significant impact. Whether you believe that COVID will have a survivorship effect or a scarring effect, it is important to consider how mortality might evolve given that the pandemic has had different impacts on different groups.

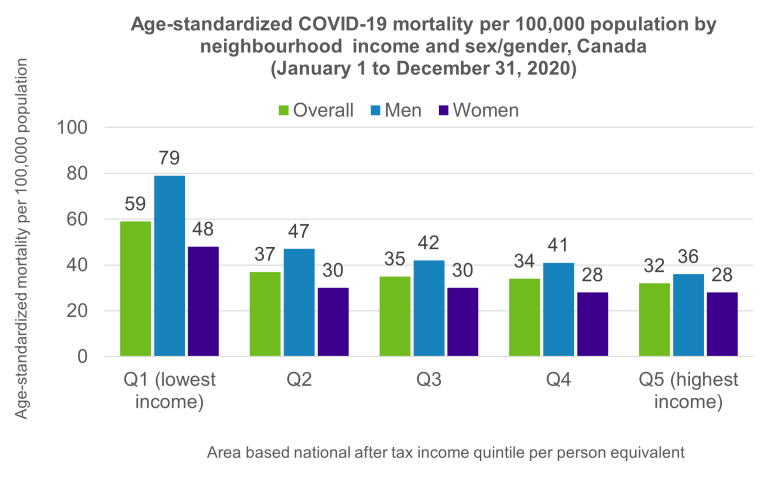

As detailed in the 2022 report published by the Public Health Agency of Canada (PHAC) titled Social inequalities in COVID-19 mortality by area- and individual-level characteristics in Canada, data suggests that the burden of the COVID-19 pandemic has been unevenly distributed among different segments of the Canadian population. The following chart shows the Canadian age-standardized COVID-19 mortality by income and gender in 2020 and highlights the prominent gap between the lowest income and the highest income groups.

Source: Pan-Canadian Health Inequalities Data Tool. A joint initiative of the Public Health Agency of Canada, the Pan-Canadian Public Health Network, Statistics Canada and the Canadian Institute for Health Information. Available from: https://health-infobase.canada.ca/health-inequalities/Indicat.

The chart underscores the following observations:

- Overall, COVID-19 mortality rates among the lowest income group were nearly twice as high as those in the highest income group;

- The gender gap in COVID-19 mortality was higher in lowest-income areas (men-to-women ratio of 1.7 in Q1 vs 1.3 in Q5);

In our previous instalment of this series, we explored disparities between population level data and Defined Benefits (DB) population data, emphasizing how the socio-economic characteristics of DB population data suggest that this group has longer life expectancies than the general Canadian population. These disparities persist for COVID mortality: Club Vita’s data set revealed an insulation effect of the DB population in 2020, with around 1% excess mortality for males and 4% for females – both significantly lower than the population levels of excess. These numbers are based on early COVID data, but they nonetheless suggest that plan sponsors and insurers might see lower excess mortality in their plans compared to the population level data.

The range of outcomes across different subgroups of the Canadian population (DB vs general population, men vs women, lowest income group vs highest income group, etc.) highlights that any adjustments for the future outlook on mortality should be considered for the specific population being modeled. Answering this question requires diving deeper into plan-specific experience and assessing the extent of COVID’s impact on a given plan.

Conclusion

Given the multifaceted impacts of COVID-19 on mortality, does the new mortality improvement scale need to be adjusted for COVID-19? The answer hinges on your outlook on the future impact of the pandemic: will pre-pandemic levels of improvements continue in the same way post pandemic? Was COVID just a bump in the road? Is there a potential scarring effect on the population or population subgroups?

Given emerging data, it appears improbable that COVID will have no impact on mortality. At a minimum, there will likely be a short-term effect that may necessitate adjustments to either the baseline assumption and/or the improvements assumption. While the CIA’s model does not currently allow for discretion in tailoring assumptions for specific populations, we think that some flexibility would be desirable. Plan actuaries should proceed with caution and consider the following key elements:

- COVID-19 has not affected all population subgroups equally. Emerging data highlights differences based on age, gender, geography and socio-economic factors. Understanding how these disparities might evolve and their short and long-term implications for a pension plan is crucial.

- Mortality assumptions are contingent on COVID outlook, whether COVID is perceived to have a transient impact, a short-term impact and/or a long-term impact, or even no impact at all. Adjustments to the baseline and/or improvement assumptions of a plan will be influenced by the expected future impact of COVID on longevity (“bounce back”, “step change”, “change in trajectory” or some combination).

- While levels of excess mortality in the Canadian DB population in early COVID years appear to be on the lower side, 2022 levels of population level mortality suggest that more recent DB mortality is likely to be more significant. Depending on plan-specific excess mortality and on COVID outlook, adjustments to a plan’s pre-pandemic assumptions (baseline and improvements) may be appropriate.

- Although data is still emerging and it is premature to make definitive conclusions, it is possible that a scarring effect on the population will emerge. We know very little about the long-term effects of COVID, but there is evidence of damage to vital organs such as the brain, the heart and the lungs. It is also possible that there could be some contributors to higher long-term improvements as a result of the pandemic. For example, from developments in medical technology or possibly some kind of survivorship effect. Practitioners should consider the balance of these effects when considering potential future impacts of the pandemic.

As the CIA state in their report, “COVID-19-related excess mortality gives rise to greater volatility and thus greater uncertainty in predicting future mortality”, we suggest that some flexibility over future parameters included in the CIA’s model may be appropriate to allow practitioners the ability to reflect a range of reasonable outlooks for future improvements.